META short-term profits vs long term vision

Welcome to UncoverAlpha newsletter. The newsletter is primarily focused on deep dives and insights into great companies in the tech and growth sector. The newsletter is free, so if you haven’t, you can Subscribe on the following link.

This article is sponsored by Stratosphere.

Gathering KPIs and segment data is a time sink for investors.

Stratosphere.io has made it easy for me to get the financial data I need beautiful out of the box graphs for my research process.

🎉Stratosphere.io just launched their brand new platform and you can give it a try completely for free.

It gives me the ability to:

Quickly navigate through the company’s financials on their beautiful interface

See every metric visually

Go back up to 35 years on 40,000 stocks globally

Compare and contrast different businesses and their KPIs

Build my own custom views for tracking my portfolio

Get started researching on the Stratosphere.io platform today, for free.

If you are interested in sponsoring the next article, you can DM and reach me on Twitter @RihardJarc

Hey everyone,

this last year Meta’s stock price shows how sentiment can drive stock prices to extremes. Almost exactly 1 year ago, Meta was trading at a market cap of $1 trillion. Today it’s less than $300 billion. The stock has lost more than 70% in a year's time frame. To make it even more for the investment history books revenue in 2022 compared to 2021, where it achieved the $1 trillion market cap so far even increased, not decreased. And to top it all at its height, the company was trading at a 25x P/E ratio (which by no means can be compared to the 2000 tech bubble where the Nasdaq’s P/E ratio hit 135x). Last year TikTok, a fierce competitor, was already present and not much smaller than it is today, the Apple iOS change was also a widely known fact, so fundamentally, not much has changed.

What did change is the perception of Meta in investors’ eyes.

Meta right now represents a battle between short-term result-orientated investors and long-term vision from a founder. And while I am not picking any side because both have valid points given the recent earnings and information about the company, I find it one of the most interesting investment cases to break down.

The breakdown of the article will be focused on the following areas:

How is the core business of Family of Apps doing?

The spending bonanza

What is reflected in this stock price?

Short-term profits vs. long-term vision what is the answer?

Is the core business dying?

Let’s start with the core business. Meta reported Q3 2022 results, and they were the following.

Revenue decreases -4% to $27.7B from $29B in 2021. On a constant currency basis, the revenue increased by 2% YoY.

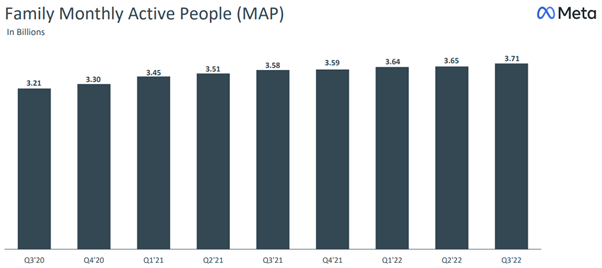

Family Monthly active people 3.71B up 4% YoY (record high)

Net income was $4.395B, down 52% YoY

Headcount was 87.314, up 28% YoY

What we can see from the headline numbers are a few important things. First of all, the narrative that has been widely spoken about that Meta’s core business is in decline and that nobody is using its core services is a wrong thesis.

Both Monthly and Daily active users on one of Meta’s properties (Facebook, Instagram, WhatsApp) are at record highs and continue to rise despite now being at 3.71B people monthly. Also, keep in mind estimates are that 5.07B people in the world are using the internet, and from that, over 1B are from China, where Meta’s services are banned. So from that, we can assume that on this scale where almost every user of the internet is a Meta user, the growth in the user base will come from growth in the human population and the increased adoption of the internet. But again, the thesis that nobody is using anymore Meta’s products is false.

From the headline numbers, we can also see revenue has started to decline on a YoY basis. There are more reasons for that. First, the macro environment is slowing advertising spending. We can see this trend in at all major advertising platforms, including Google, Snapchat, and others. Meta had to overcome the ATT problems caused by Apple’s iOS privacy change which, according to their estimates, costs them $10B in 2022 or about 10% of revenue. And the third reason for the decline in revenue is the transition of Meta’s Instagram and Facebook assets to more short-form videos also called Reels. Because Reels is in its early days, it is much less monetized as Meta’s News Feed or Stories medium and is, according to their latest earnings report causing a $0.5B revenue headwind each quarter.

Meta is prioritizing pushing Reels because they see the future of social media in a more short video format and because this is increasing engagement on their platforms.

And then the last important takeaway from the headline earnings numbers we can see is rising costs and, with-it lower profitability. This can be seen both in a decline in profit and a significant increase in headcount. While we will get to the cost side later in this article, I want to summarize the main reasons for the growing costs:

Increased investment in data centers and chips for the AI recommendation engine.

Investing in the AR/VR and metaverse concepts

“after effect” from the rapid growth of e-commerce in the pandemic, which bloated headcount

But even more interesting than the headline numbers were what was discussed on the earnings call and produced a clearer picture of where Meta’s core business is and where it is going.

As we mentioned before, users are at record highs both in terms of daily and monthly activity. What is even more encouraging is that engagement and time spent are also on the up path, and this is not just in the countries outside of the US but also in the US:

“Specifically, in terms of aggregate time spent on Instagram and Facebook, both are up year-over-year in both the U.S. and globally. So while we're not specifically optimizing for time spent, those trends are positive”

David Wehner (CFO)

The reason for this is that short-form video is more addictive to users. Users spend even more time on Instagram and Facebook because of Reels. Despite TikTok bringing competitive pressures to Meta, it also opened a new path for the company with potentially higher long-term engagement rates than before. What most social media investors know is that higher engagement, in the long run, translates into higher ARPU and, with-it higher revenue.

We also got user metrics for all the apps when it comes to active users:

Facebook – nearly 2B users daily

Instagram – over 2B users monthly

WhatsApp – over 2B users daily

What was even more encouraging for investors is that Meta is finally putting its focus on pushing and monetizing WhatsApp to its full potential.

WhatsApp is the next growth driver.

While we all know WhatsApp is the key app when it comes to the Indian economy and its users, it was a positive shock to hear from Mark that WhatsApp’s highest-growing region in terms of users right now is North America.

When it comes to WhatsApp monetization, it’s in its early days and growing fast with click-to-message ads, which grew over 80% YoY. Click-to-Messaging ads are the primary way Meta plans to monetize WhatsApp:

“We started with Click-to-Messaging ads, which let businesses run ads on Facebook and Instagram that start a thread on Messenger, WhatsApp or Instagram Direct so they can communicate with customers directly. This is one of our fastest-growing ads products, with a $9 billion annual run rate. This revenue is mostly on Click-to-Messenger today since we started there first, but Click-to-WhatsApp just passed a $1.5 billion run rate, growing more than 80% year-over-year”

Mark Zuckerberg

It is no surprise that Zuckerberg, just a few days ago, in a talk addressed to Meta employees, said that Business messaging is their next big growth driver:

"We talk a lot about the very long-term opportunities like the metaverse, but the reality is that business messaging is probably going to be the next major pillar of our business as we work to monetize WhatsApp and Messenger more,"

Mark Zuckerberg

And this plan makes sense. As Meta properly assessed, people shifted the way they use and consume social media nowadays. Social media users went from being active publishers of their lives and publishing it to everyone out there in the universe to more passive consumers of content in “the public” from other people and then sharing that content and views in more private channels. The private channels are either messaging to friends and family or participating in groups that have an aligned interest, such as Facebook Groups, WhatsApp groups, etc. In Meta’s future world, the foundation is simple, users consume content from third-party (influencers, micro-influencers, and social connections) via Reels, Stories, and Feed but engage and share those content on private channels (Messenger, WhatsApp, Instagram DM).

With that said, how is the answer to TikTok Meta’s short-form video Reels doing since this is an important part of Meta’s future flywheel?

Reels gaining traction

We got a clear answer on the call on this topic as well:

“This of course includes Reels, which continues to grow quickly across our apps -- both in production and consumption. There are now more than 140 billion Reels plays across Facebook and Instagram each day. That's a 50% increase from six months ago. Reels is incremental to time spent on our apps. The trends look good here, and we believe that we're gaining time spent share on competitors like TikTok”

Mark Zuckerberg

This was the first call in which Mark stated that Reels is taking market share from competitors like TikTok and, as such, should be a very important indicator for investors. Now while you can take this statement with a grain of salt, there is a fundamental reason why people would prefer to consume short-video content via Meta’s Instagram or Facebook platform than to go to TikTok.

At the Dealbook conference this week, Mark also said that Reels has half the usage of TikTok (outside of China) already, which is up from what was somewhere in the teens a year ago.

First of all, Meta’s long stood competitive advantage in the social media space was its vast social graph which people built on their platforms. In essence, nobody wants to go somewhere else and start looking for the people they know to “add” to their network from scratch. The only demographic that proved multiple times in history so far that they were willing to do that are the kids and teenagers. That is because they are “building their social graph” from zero anyway. This is also the main reason why you see fast adoption in newer platforms like TikTok and Snapchat from kids and young people. But the thing that Meta needs to do right now is the same thing it did with Snapchat when it released Stories. When Meta cloned Stories from Snapchat and put them on their platforms, they didn’t steal the users that were on Snapchat, but they stopped the people that were on Meta’s assets from going to Snapchat. Meta doesn’t need to take the users from TikTok the only thing they need to do is remove the need from their existing users to go to a platform like TikTok. And with it, the social graph advantage is still in place. People still want to look at what their friends and family post, but because these people post less in between, they want to watch content from people they don’t know that do post content (third parties, influencers, etc.).

In my view, there will always be the need to have and use Instagram or Facebook because if you are an adult, you don’t want to go through the hassle of building your social graph from scratch, and at the same time, you don’t want to use more apps that offer the same functionality. Your time as an adult in the online world is more limited than your time when you are a teenager; that is why you are more careful about what you use.

Meta and TikTok can both live together, just as Meta and Snapchat are today.

But there is a difference in value, having different demographics of people use your platform. From an investor standpoint, having a user base that is more mature is also more valuable because of two reasons:

The more mature audience has bigger spending power. Because of its advertisers, it’s a much more valuable audience.

Taste, when it comes to kids and teenagers, changes a lot both in terms of when they grow up but also in terms of generational changes. What we have seen is that teens change their preferred usage of platforms every few years. They even prefer the ones that their parents are not on. From an investor perspective, that means risk when owning a platform that teens are using today because it doesn’t mean that they will use it in the next 3-5 years. This is what is happening to Snapchat today with the rise of TikTok, and it is what I believe will happen to TikTok in the next 5 years.

How is TikTok doing?

Looking at the data from TikTok recently, it doesn’t seem like the company is without its troubles in this environment. Earlier this month, TikTok reduced its global revenue goal by $2 billion or 20% for 2022 to $10 billion from $12 billion as the economic environment worsens for digital advertising. On top of that, just a few days ago, the Information reported that investors in TikTok are struggling to sell their shares in the secondary market even at a $240 billion valuation which is 20% below where Byte Dance recently bought back stock.

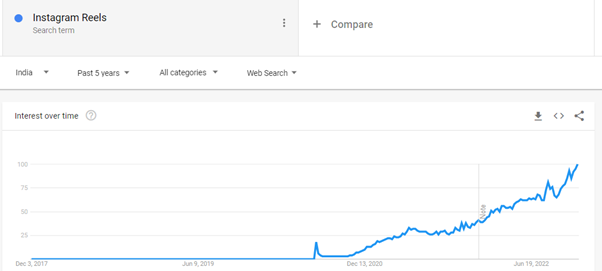

Another big dark cloud hanging above the company is regulatory scrutiny, especially in the US, as lawmakers are looking very closely into how TikTok is handling US user data as what many could be a potential national security risk with China potentially having access to US users’ data via TikTok’s parent company Byte Dance. In recent months this pressure has been increasing, and a resolution to this seems to be on the table in the coming months. For similar reasons, TikTok was banned in India in 2020, which was and still is a big hit for TikTok since India is one of the fast-growing regions in the world both in terms of people and development. After the ban in India, Instagram’s Reels took momentum and lured the creators and the ecosystem. For that reason, together with WhatsApp's strong presence in India, the country is one of Meta’s most important regions. The search data for “Instagram Reels” in India shows a clear and strong pattern of high growth since its launch in 2020.

There are also signs that the rapid growth in TikTok is starting to slow down substantially since the pandemic. According to Sensor Tower data as reported by Morgan Stanley, total time spent in the US is starting to plateau:

The spending bonanza

One of the main issues investors faced, especially in this earnings report from Meta, was the higher costs when it came to 3Q but more so of what management had to say for OPEX guidance for next year. This was the key thing for the stock market reaction after the results:

“We anticipate our full-year 2023 total expenses will be in the range of $96-101 billion. This includes an estimated $2 billion in charges related to consolidating our office facilities footprint.”

And this:

“Reality Labs expenses are included in our total expense guidance. We do anticipate that Reality Labs operating losses in 2023 will grow significantly year-over-year. Beyond 2023, we expect to pace Reality Labs investments such that we can achieve our goal of growing overall company operating income in the long run.”

This is the piece that caused the stock to go higher in the pre-market after earnings came out to go much lower after it. It shook investor confidence that signaled that despite the macro slowdown, Meta has no intention to slow down its spending and investments and that Mark Zuckerberg, given his super-voting power, does not care how investors & the stock price reacts in the short term.

But what are all these investments Meta is making?

In essence, it comes down to two main areas. First, Meta is in an investment cycle building out its AI and infrastructure capacities. And the reason for that is because of the iOS privacy change and the rise of content viewed from third parties (outside of your social network). There is an increasing need for AI solutions. Meta is leaning strongly toward AI prediction algorithms that require fewer user data to get them better accuracy on ad targeting now after the signal loss. This means Meta has to build out the hardware infrastructure to be able to process and run these algorithms. The other trend, as already mentioned, is the rise of third-party content. Content like short-term videos is produced by a random person in the world. This means that the Instagram and Facebook algorithm needs to consider not only content that your social circle (your connections) has produced but content from all over the world that is being produced and recommend that content to you based on meaningful predictions of what you might like. This, again, requires strong AI and hardware capacity to be able to run these algorithms for over 3.7B people monthly. Because of this change in the last 2 years, Meta has become one of Nvidia’s best clients. But these investments can give Meta a big advantage in the coming years as smaller competitors do not have the resources to build out this kind of infrastructure and will have to rely on public cloud providers which won’t be able to fit the needs of these use case perfectly the way Meta can because it fully owns, controls and develops the infrastructure. When it comes to recommendation AI engines, both in terms of serving ads or content, the company that has the best algorithms will perform better as both advertisers and users will be happier with better-curated content for their needs and wishes and better-performing ROIs on ads.

The second area of big investments is the AR/VR and metaverse area. Now I won’t go deep into what the metaverse concept is in this article, you can check my previous article for that. For a clearer picture, just a few days ago, in a letter to employees, Mark said that about 20% of Meta’s investment budget was going to Reality Labs. Within the budget, the breakdown for the segments is the following:

50% for AR

40% for VR

10% for virtual social platforms like Horizon Worlds

While we can argue about the future prospects of these investments, to me, the most important one is AR. AR has the prospects of being the next computing platform like the smartphone. And this is not a belief that is shared only at Meta but also what a lot of other big tech companies see as the future. Including companies like Apple, Nvidia, ByteDance, and many others.

But to have the best working product for mass adoption when the time is right, Meta needs to build technologies that will be used by the AR smart glasses. And these technologies are being built today at the company both in terms of the VR efforts but also technologies like the EMG wristband and others. The strategy at Meta is quite clear, develop technologies that are today used in VR but will be important for the AR product. We all know for AR glasses to be mass adopted, they need to be, first of all, sleek and not heavy (look like normal glasses), and they need to be powerful in both the software sense and also when it comes to speed (hardware and chips). Technologies like the EMG wristband also need to be developed so you will be able to use this new gadget not only with voice commands but also with your hands, which is also the primary way we have used other computing platforms so far, like the PC or the smartphone.

While the verdict of these investments in the AR/VR segment will bare fruit in the coming years is still out there, it is probably one of the most exciting consumer innovations in a long time. Big tech is finally stepping away from just buybacks and hoarding cash.

So Meta is not ready to make cost controls?

As we talked about before, after the earnings call, investors lost confidence in cost controls and believed Mark was in his own world and did not listen to investors….but as with many things in life, “The soup is never eaten as hot as it's cooked.”

A few days after the earnings Mark came out with a letter addressing both employees and investors.

The letter shows an important step that Mark is, in fact, hearing investors and is starting to address the cost concerns of investors. In the letter, Meta announced layoffs of 11.000 employees or 13% of the total workforce. The layoffs were both in the core business segments but also in Reality Labs. But besides the layoffs, Mark addressed the cost controls side head, saying that in this environment, they need to become more capital efficient. Cutting costs like scaling back budgets, reducing perks and real estate footprint.

With it, Meta also reduced their overall expense guidance for 2023 from the $96-101 billion set a few days ago to the new range of $94 – 100 billion.

Besides the layoffs, Mark also explained that they are currently making a thorough review of infrastructure spending, hinting at possible cuts there as well. Infrastructure, as we know by now, is one of the main areas of CAPEX for Meta.

For me, the letter shows an important step from Zuckerberg. Even though investors might want more cost cuts (and maybe we will get them in the coming months), the real result here is the willingness of Mark to accept the current macro situation and listen even to short-term shareholder requests for profit. Probably one of the main reasons for doing so is the stock price drawdown which by itself does not fundamentally affect the business performance of the company, but when a stock price drawdown is so big, the company can get problems attracting future talent as stock-based compensation is one of the main ways tech companies reward employees. On top of it, Meta went from the $1 trillion club to a market cap of under $300 billion. Given its ambitions and future plans, Meta needs to remain in a position of strength both when it comes to the capital and willingness of talent to work and also when it comes to public perception.

What is reflected in the stock price?

The company is currently trading at $120 per share, which is equivalent to $319B in market cap. The company made $39.37B in net profit in 2021, but since we mentioned the rise in costs, this year looks to be a year where they will earn around $23.5B (if Q4 is similar in trend compared to Q3 vs. last year). Given the headwinds faced in the second part of this year already talked about in this article, revenue is going to be similar to what it was in 2021, so near the $118B mark. This would give them a current P/E ratio of 13.5x and a Net income margin of 20%.

If we look at the historic Net income margin of Meta since it became public and especially since it matured as a company from 2016-2021, its Net income margin was in the 30%-40% range.

Taking into consideration the recent Opex guidance for 2023 of $94B-$100B if revenues stay fairly the same in 2023 and Meta doesn’t do additional cost cuttings, its expected net income in 2023 is in the $24B-$18B range, which also includes a one-time $2B charge related to the consolidation of office facilities footprint. Net income from continued operations should be in the $26B-$20B range. If we take the midpoint of that range, the company is still trading at a 13.8x forward P/E ratio with a historically low net income margin of 20% or below. Even if revenues were to decrease in the first half of this year, given the bloated costs, Meta has more than enough room to reduce costs.

We know, given Meta’s history, that they can manage a net income margin of 30%-40% if they want to. Even if we take into consideration an event like a severe macro slowdown and the company’s goal of still investing a substant amount into their investments like the Reality Labs, a 25% net income margin is more than achievable and fully in the hands of management. If revenue were to slide by -20% next year in this severe scenario (which is not nearly my base case), the 25% net income margin would still bring Meta to $23.6B in net income and value, the company at the same low multiple of 13.5x P/E.

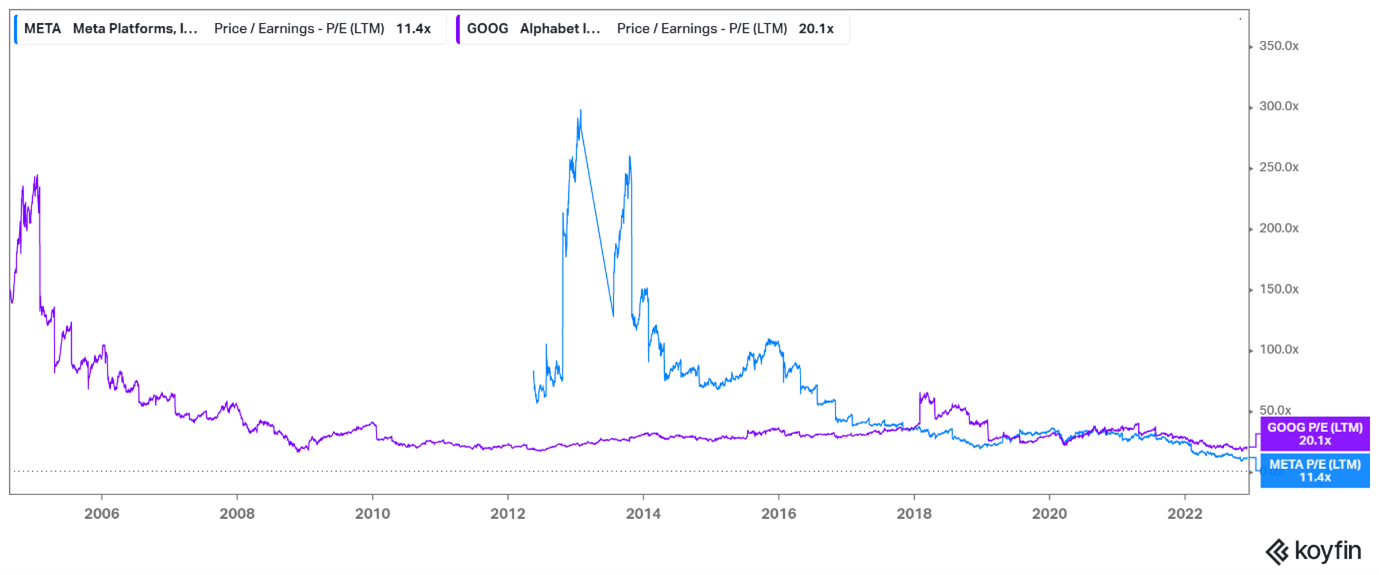

Since it became public, Meta’s P/E ratio has never even come close to the levels that we are seeing today. Nor has Google, which has a longer history of being a public company than Meta. The lowest P/E multiple for Google was at the bottom of the 2008 recession, with a 16x P/E ratio.

In my view, the multiple is extremely low at this point and gives zero value to the investments they are making at Reality Labs and, at the same time, underestimates the long-term capabilities of Meta’s net income margin. Meta also has more cash on hand than the sum of total liabilities, so the balance sheet does not affect the valuation negatively in any way.

The future and the stock price at these levels are, in my view, in full control of Meta’s management at this point, even in a severe macro slowdown/recession.

There is not much Meta has to do for the company to achieve a much higher market capitalization. If they reel in some costs and bring the net income to a 25% level (still giving more than enough room with future investments like Reality Labs) and with no severe economic recession, the company would make $29.5B in net income with a growing business, and a more normalized P/E ratio in the 16-18x range even with interest rates at 4-5%. The company would be a $500 billion company at that valuation mid-range which is 57% higher than it currently trades at. And again, even in this scenario, Meta is still in full investment mode when it comes to their future plans, and the valuation still presumes 0 value to Reality Labs which could change quickly in a few years.

Let’s not forget that revenue growth of the core business will, in my view, return as WhatsApp starts to contribute meaningful revenue and as Reels higher engagement and bigger times spent by users drive more revenue to the company and becomes a tailwind, not a headwind. Not to mention the world’s macroeconomic headwinds will ease and turn into tailwinds in the future and digital advertising still has a long and very healthy future, given its effectiveness compared to other types of advertising. Even a 10% higher revenue could contribute almost $8 billion to Meta’s bottom line, which is more than 30% of today’s net income.

Short-term profits vs. long-term vision, what is the answer?

There is an active dilemma regarding Meta right now, and it has to do with two things. One is investors have become 100% focused on results that are going to be delivered the next quarter from companies as the current macro environment with rates, inflation, and recession is causing them to forget about the long-term metrics and future of companies.

The second thing is Meta still has a founder, CEO Mark Zuckerberg whose vision and plans at Meta are big and bold. And the combination of these two different goals is causing a clash that is reflected in the stock price.

It's clear from the results that the narrative of nobody using the company’s core services or that it is in terminal decline is false. In fact, the numbers show there is a record high number of users using Meta’s services on top of it, engagement is rising because of new formats like Reels, which are more addictive. One year ago, Meta’s stock price was at record highs, and there I would argue, things looked worse than today (leaving macro aside). One year ago, TikTok was as big and as strong of a competitor as today, the iOS change was already known, and Meta had two-quarters of results since the change, Meta’s services had fewer users than they have today, Reels had less traction. So, what changed? One is the macro (but the difference in drawdown compared to Nasdaq is much bigger), the other is Meta continued to invest and hire people (which is a problem they are addressing now), and the third is the narrative changed because of the stock price declined. But long-term investors should understand price drives narrative in the short term, but in the long term, fundamentals take over.

While I agree with many investors like Brad Gerstner from Altimeter Capital urging Meta to do more on the cost side and make Meta a leaner organization, I also understand and, as a shareholder, want Meta to invest in new technologies like AR/VR. The key to new technology is to be ready and to time it perfectly when the market is ready. The biggest moment for all the investments in the Reality Labs segment will come down to when Meta launches their smart glasses called Nazare.

Both investors urging for cost-cutting as well as Mark as the CEO have good points. The key for the company in the short and long term is to strike a balance between these two views. With just a simple, clear letter, Mark could give investors confidence that Meta won’t go past a certain profitability when it comes to the whole company and ratchet down costs and investment if macro puts Meta in that position. Investors would see that as a sign of stability and continue endorsing investments in the Reality Labs segment, knowing it has its limits in terms of cash burn, which are dependent on the performance of the core business.

The last letter sent by Mark addressing these issues is the first step in this direction and shows a much different tone than it was on Meta’s last earnings call. I think by now Mark understands that if you have such a big drawdown in your stock, this is not only the “problem of investors” but also of the company as it’s harder to attract talent and reward talent (SBC) at the same time Meta wants to be perceived in public as a dominant leading technology company. They want to be in the same conversation when it comes to size, influence, and market cap as the Apples, Googles, Amazon’s and Microsoft’s of the world and not the Cisco’s, Salesforces, and Oracles of the world. No harm intended to these companies, but it’s another league.

Now obviously, I am biased since Meta is also one of my portfolio holdings, but my view is that Meta, despite being thrown all these problems, still has all the answers for these problems and, more importantly, the tools to help overcome them and become an even more fierce company in the future. And for long-term investors, it’s another important lesson - listen to the numbers and not the narrative.

If you haven’t yet, feel free to subscribe to this free newsletter & share. If you feel so, I would really appreciate it if you shared the link to the article on social media, as this is the best way to find new subscribers to UncoverAlpha and keep the newsletter free for everyone. Thank you very much all!

Disclaimer:

I own META stock.

Nothing contained in this website and newsletter should be understood as investment or financial advice. All investment strategies and investments involve the risk of loss. Past performance does not guarantee future results. Everything written and expressed in this newsletter is only the writer's opinion and should not be considered investment advice. Before investing in anything, know your risk profile and if needed, consult a professional. Nothing on this site should ever be considered advice, research, or an invitation to buy or sell any securities.

Comprehensive and balanced, great job Rihard.

I can’t wait to see WhatsApp evolving.