Pinterest analysis: The social commerce disrupting e-commerce!

This is an analysis of Pinterest, one of my biggest portfolio positions. I did several Pinterest analyses and shared it with UncoverAlpha subscribers back in the day when this was a $20 stock, but I feel it’s the right time to give you an update and maybe even dive deeper into some of my investment thesis points.

The story of how it began

Pinterest was founded back in 2010 by Ben Silbermann, Evan Sharp, and Paul Sciarra. What you may not know or expect is that Pinterest, when it launched, didn’t skyrocket right away. In fact, after 4 months of its launch, Pinterest had only 200 users. Because of the low userbase unconventional social media approach (no news feed etc.) and founders without an engineering background, they had trouble getting fundraising.

Pinterest was also for 2 years after launching an invite-only platform. That limited its potential for user growth but allowed the founders to build out an initial community and prepare the product for international success.

The Platform

Now Pinterest is one of the biggest social media companies in the world. The platform is primarily designed for people to search for ideas, inspirations, hobbies, and passions. Thus, the users that come to the platform are much more focused on what they want to get from using it. This has increased in the COVID era, as we can see from Pinterest’s latest remarks on their Q3 earnings call:

“We’ve learned more about the users who began using Pinterest during the COVID-19 period. First, their engagement tends to increase when lockdown orders are in effect and wane when the orders are lifted. Second, they typically come to Pinterest for a specific purpose (e.g., building a home office) rather than for general inspiration. This means they tend to search more than older cohorts, a new-user trend that pre-dates COVID but that has accelerated since March. More searching on the platform raises the bar on serving relevant results (particularly more relevant ads), but search engagement also tends to have higher commercial intent, which represents a big opportunity for future growth, particularly as advertisers increasingly seek platforms that are able to deliver sales and conversions.”

With that in mind, Pinterest is the perfect social commerce company. Its main growth opportunity, in my opinion, is its ability to feed and connect with e-commerce and present people with a perfect online shopping experience.

The platform also has a much more friendly vibe than many other social media platforms as people are not searching for any political topics or news-related things. With that, it means that advertisers have a lower “reputation risk” that may occur from a social media company being caught up in a political or social debate.

The things that are most searched on Pinterest are related to furnishing, home décor, jewelry, cooking, etc.

Users

3.1. Demographic

An important thing to analyze with Pinterest is its user demographics. Pinterest has done a great job capturing the population that is most receptive to shopping and has the household buying decision:

– 71 % of Pinterest users are women. Pinterest captures 83 % of all US women between the ages of 25 – 54.

But the users are not only women:

– 40 % of US dads use Pinterest for searching, shopping, and planning for fatherhood.

Dads normally search for DIY projects they can do with their kids and look for ideas on how to prepare healthy meals and stuff like that.

We have to acknowledge that this is probably the “prime audience” to capture as a social media company. Young women are the ones that make 80 % of buying decisions in the US household. On the other hand, we all know that people with children are in the period of their life where they spend most on things that children need, buying a new car, buying a new home, etc. These are statistically the ages where most people make their biggest lifetime spending decisions. And people tend to be less price-sensitive when making these big purchases.

3.2. User behavior:

Another important data point to consider with the users is their behavior.

Staggering data point to consider about user behavior:

“ 89% of US Pinners use Pinterest for inspiration in their path to purchase. And it’s not just inspiration that consumers are looking for. 47% of Pinners log onto the site specifically to shop, making it nearly four times more effective at generating sales than other social platforms. “ Source: SproutSocial

Even more interesting is this table here:

From this table, it is clear that Pinterest is “THE” best fit for social commerce currently as it is the leader when it comes to being used for Finding/shopping for products compared to other social media like Facebook, Snapchat, Twitter.

Another interesting data point SproutSocial puts out is that People on Pinterest rate ads on Pinterest 1.4 times more relevant and useful than those on other platforms. That means that because of the way they use Pinterest, these users don’t mind ads; in fact, if they are relevant, they even like them. Users that like ads on a social media site are infrequent and valuable.

With everything said, we have to acknowledge that time spent on the platform is probably lower than with other social media sites. For example, the average time spent on Facebook is around 38 minutes per day, while there is no exact data on the average time spent per day from a Pinterest user SproutSocial states that the average time spent per session on Pinterest is 14.2 minutes.

3.3. User growth

Pinterest has been growing like crazy. This is especially the case in 2020, where COVID and lockdowns affected the whole world.

In Q2 2020, the MAU YoY growth rate has been 39%, and in Q3, it was 37%. Now, these numbers, when put into the context of the current user base, show an even stronger picture. Pinterest's user base is growing in the 30-40% range, with 442 million users already on the platform.

But not only has there been an acceleration of user growth, but user engagement rates have also accelerated. While we must acknowledge that a lot of the user engagement increase has been driven by lockdowns, Pinterest management noted on their earnings call back in Q2 that user engagement stayed elevated before pre-COVID times also after the lockdown restrictions eased into the early summer.

“The people who began using Pinterest during COVID-19 continued to have high levels of engagement even after shelter-in-place restrictions were eased. In fact, new users in the COVID-19 cohort are currently more engaged than a cohort of new users during the same period last year”

This provides important information for investors on what to expect after COVID.

Financials and Monetization

Now let’s look at the financials and the monetization efforts of the company.

Pinterest has seen an acceleration in revenue in the last year and has improved its healthy gross margin.

A revenue breakdown quarter by quarter in 2020 shows a better picture.

Pinterest had a good start of the year but got hit by the pandemic when advertisers decided to pause and stop expenses such as marketing spending. This resulted in a 35% revenue growth for Q1 and 4% revenue growth for Q2. But as advertisers got rid of fears of an economic catastrophe and saw COVID as the new normal, they continued their marketing spending and even increased their budgets as doing business online is almost the only way you can do business nowadays. This resulted in a huge revenue increase of 58% in Q3. Now Pinterest’s most important quarter of the year is the fourth quarter. Pinterest will report Q4 results on the 4th of February after the market close.

Pinterest guided for Q4 revenue growth on the last earnings call to be at 60%:

“Our current expectation is that Q4 revenue will grow around 60% year over year, a modest acceleration compared to our growth rate in Q320. We continue to navigate uncertainty given the ongoing COVID-19 pandemic and other factors.”

If they hit their guidance, Pinterest will close the 2020 year with approx. $1.6B in annual revenue.

Also, when looking at the balance sheet, we can see that Pinterest has built a nice war chest of cash as they have around $2B in current assets and $0.36B in total liabilities. This can further provide them the ability to invest in bringing new features to the platform as well as fueling growth and possibilities on the M&A side.

4.1. ARPU

As with any social media company, it is important to look at the ARPU numbers.

Pinterest is still in its early days regarding monetization of its user base, and with high user base growth numbers, I prefer to see the company focusing its efforts on continuing this growth in user base than to overly focus on monetization.

We can see that the main driver of revenue so far is coming from users in the US as international expansion is in the early days. But looking at the user growth of international users, we see that this is the fastest-growing segment.

Management also acknowledges that the biggest opportunity in terms of monetization is in the international base:

“U.S. ARPU was $3.85, an increase of 31% year over year. International ARPU was $0.21, an increase of 66% year over year. International ARPU remains in the early stages, as we have only begun to execute on our strategy to provide ads that are useful and inspiring to our users in regions outside of the U.S.”

Another big factor to better monetization should also be the fairly newly introduced auto bidding option.

“Automatic bidding for conversion objectives launched at the beginning of July and in Q3 represented more than half of conversion revenue, and automatic bidding for shopping ads launched in September. In addition to spending their existing budgets more efficiently, the majority of early adopters of oCPM automatic bidding have increased their budgets on Pinterest”

Having an effective platform for advertisers in the monetization phase of the business is key, as we learned from the Facebook playbook. Although Pinterest is still early in this regard, its focuses can lie elsewhere for the time being.

Social commerce

Social commerce is the biggest opportunity, in my opinion, for Pinterest. In essence, social commerce means that the user is on social media the whole cycle of the shopping experience. So from the discovery phase to the end, buy and enter your shipping details phase. It is very popular in China, and the East as companies like Pinduoduo in China and Shopee from Sea limited have built great businesses around it.

On the West, really the main two “assets” for building a social commerce experience are Pinterest and Instagram. And as we saw from the user behavior numbers, Pinterest’s platform is made for this.

Social commerce is one of the areas Pinterest has been focusing on a lot, and rightfully so. The first step was introducing the Buyable Pins, now partnering with companies like Shopify. All of these things add to the shopping experience of the users. And obviously, the users are behaving well to these new Shopping features, as we can see from the earnings call:

“We also launched new product pin detail pages that include alternative images, shipping information, sale pricing, and more. In addition, we recently announced a new suite of merchant tools including an updated merchant storefront profile, testing for product tags and a more intuitive catalog feed ingestion tool. These efforts, along with the features we’ve launched over the past several quarters are making a difference; the number of Pinners engaging with shopping surfaces has grown over 85% in the six months ended September 30.”

With Social commerce features, Pinterest can expand its revenue from ads. And the technology that will be essential for the coming future in this field is AR and holograms. Both Facebook, as well as Pinterest are going in this direction. As shopping will mean that you will be able to project new makeup on your face and see how it looks, or clothes and also being able to put holograms of furniture into your house and see how these elements would look in your environment. We can see Pinterest’s start in this field with its latest AR-powered try-on experience for eyeshadow. More info here: Pinterest launches an AR-powered try-on experience for eyeshadow | TechCrunch

Pinterest has also moved significantly into visual search, where people can take or upload a picture of a product, and Pinterest’s algorithm will find similar matches. It is really doing all the right things with the trends that are going on in the e-commerce and social commerce field. They also announced a partnership with Zoom for Pinterest online classes.

Valuation

So from a valuation standpoint, I started my Pinterest position back when it was in the $20 range and since added on almost every bigger pullback. The company now stands at $73 and a market cap of $45.17B.

If we calculate a simple P/S ratio and estimate that Pinterest 2020 revenue will be $1.6B, we get to a 28 Price to Sales ratio with revenue growth in the 50-60% range.

While that might seem high, I like to value social media companies in their “growth phases” more based on the user base as monetization has not kicked off fully yet.

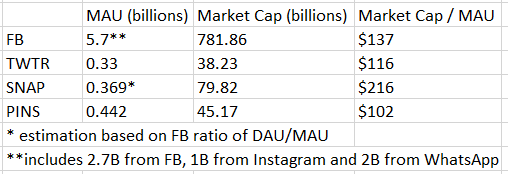

So here is the calculation:

We can see that according to the current market cap, a PINS user is valued at $102, while for comparison, a Snapchat user is $216 and a FB user is at $137.

Now keep in mind that from the user demographic segment of the analysis, we saw that Pinterest users should be even more valuable than users, for example, from Snapchat, which are mostly teenagers. Teenagers don’t have as much buying power and are less likely to buy products of bigger value. While platforms like to see teenagers using them and believing this will continue when they grow up, I don’t buy this theme completely. In a phase where you are a teenager, you are developing and changing habits very fast, so I don’t believe there is that high of a chance that you will stick to a platform that you used for sending memes and jokes to your highschool friends for buying your furniture when you buy a house.

We also need to take into account the growth of this user base. From all the mentioned companies, Pinterest is the only growing user base in the 30-40% range. For comparison, Snapchat’s recent user growth was at 18%.

My fair value for PINS, given all the above, would be to value a PINS user somewhere between a value of a Facebook user and a Snapchat user. That would mean between $137-$216 per user.

That would translate into a PINS market cap of $60B- $95B. Given PINS market cap is now $45B, it is obvious I see the stock going much higher in the mid to long term horizon.

Summary

PINS is one of the most important companies in my portfolio, and I believe it will continue to be in the future. It is performing great in terms of growth; it has big potential in the social commerce segment and looking at a more long-term picture, it is one of the most important assets for e-commerce companies that will compete against Facebook in the future. By that, I mean companies like Etsy and even Amazon. When social commerce takes off, these e-commerce companies will have to look to participate in PINS either via a partnership or even M&A, as building out a big social media company is one of the hardest things to do, even if you have deep pockets. Pinterest already accounts for 40% of Etsy’s social traffic.

Copying a platform like Pinterest is not that easy as Facebook already tried with their project called Hobbi (more about it here https://techcrunch.com/2020/06/30/facebook-shuts-down-hobbi-its-experimental-app-for-documenting-personal-projects/), which they shut down.

I am staying long the company, and as long as I see user growth, albeit even at a slower pace than in 2020, it is enhancing my conviction in the stock. In social media, if you have the users and they keep coming, the advertisers will naturally follow.

If you liked this analysis and are interested in others, please subscribe to this newsletter; it is free. I also regularly post my portfolio positions and the investment moves I make.

Disclaimer:

Nothing contained in this website and newsletter should be understood as investment or financial advice. All investment strategies and investments involve the risk of loss. Past performance does not guarantee future results. Everything written and expressed in this newsletter is only the writer's opinion and should not be considered investment advice. Before investing in anything, know your risk profile and if needed, consult a professional. Nothing on this site should ever be considered advice, research, or an invitation to buy or sell any securities.

You are the best

now the market cap to mau is $80.18