Square the next generation bank - analysis

I had recently added a new position to my portfolio when the market was volatile two weeks ago and the stock dipped below $200. The company is Square (SQ). This is the summary of my investment analysis regarding the company and the stock.

Breaking down Square has two main pillars of their business:

- Seller ecosystem

- Cash App

Seller Ecosystem

What is Square Seller Ecosystem?

Seller ecosystem is a B2B offering of Square. It is how Square started. The seller ecosystem started from a simple idea of easily handling card payments by businesses from customers. Since then, the ecosystem has evolved completely, and now Square offers solutions such as online store creation, checkout links, contactless payment options, e-commerce APIs, POS services, and hardware. They also offer services to businesses such as business loans, fund transfers, payroll services, and very popular lately business debit card.

Square B2B business has been affected by the recent pandemic as a lot of their customers on the POS side had to stop their businesses. But on the other side, a lot of their online business grew because businesses were moving online and using Square online services.

At first glance, you might think that this business segment constitutes a lot of hardware sales, but in fact, Square B2B has grown to a fully grown service business, with hardware sales representing a minority of the total revenue generated by this segment. In fact, in the last reported Q3 2020 quarter. Hardware sales were only $27 million out of $965 million that the whole segment generated. So less than 3%.

Performance of the segment

Despite the effects of the pandemic, the segment is performing well, with online businesses adopting more and more of their features and upsetting the loss of revenue generated from on-sight business solutions (such as POS).

In the last quarter, revenue from the seller ecosystem generated $965 million in revenue compared to $918 million in the same period last year. So despite the pandemic, the business segment grew 5% YoY. The main driver for the growth was Transaction-based revenue representing over 87% of the segment revenue now. On the Transaction based revenue side, the segment that is most interesting to me is this one:

Source: Square Q3 earnings report

But also on their Subscription revenue, despite it dipping 6% YoY, the dip was related to Square Capital offering fewer loans while other subscription services grew 28% YoY.

Another positive factor is Square’s business debit card offering. Many businesses found out that getting funds as fast as possible is an important thing, and now Square noted that 50% of new clients that come to Square B2B offering in 1-month order also Square Business Debit card.

Looking at this segment, I can’t shake off the feeling that I am looking at a well counter correlated business that looks to some extend similar to Disney. While the pandemic hurt parts of Square’s B2B business in terms of POS (like Disney theme parks), it accelerated the online parts of Square’s B2B offering like Square online and eCommerce API (similar to Disney+).

Valuation

Looking at trying to value this segment. First of all, we have to acknowledge that it is not a hardware company as less than 3% of the business segment revenue comes from hardware. In fact, Square is losing money on the hardware segment as hardware is a way to gain new clients to start using Square business services.

If we look at the recent data, the business is on track to generate around $3.7B in revenue annually. While in the last 9 months from Q3, the YoY growth was 0%, with the pandemic stabilizing, we can expect the numbers in terms of revenue growth to start rising again in 2021. The last quarter showed a 5% growth, but I think it is safe to assume once also the POS business starts getting back to normal, we can expect revenue growth to be in the 10-20% range. The business also generates a 45-50% gross margin, which is not extremely high but still very healthy (for comparison, Twillio generates a 50-55% Gross margin).

With 10-20% revenue growth and a 50% gross margin applying a P/S ratio of 15 would be more than appropriate given current market conditions. With that multiple, the Seller ecosystem segment is worth $55.5B.

Cash App

What is Cash App

I will not go deep into what Cash App is and what they offer because I think most people are familiar with it, and it would add no value. I think it is important to highlight from this Fin-Tech wallet product that they have evolved far more than just P2P payments and basically build out a Fintech bank out of Cash App (very similar to SoFI). So the main drivers for revenue growth for CashApp are monetizing products such as brokerage, investing, crypto investing, direct deposits, debit cards, etc. The P2P transactions feature of CashApp actually makes a loss for Square. They say it is their marketing cost and helps them with onboarding new clients.

Performance of the segment

The CashApp is a real monster when it comes to FinTech super apps. The last number on the active user count is over 30 million users. Although some reports say, they already had over 40 million users in 2020. The app is offered in the US, Canada, UK, Australia, and Japan. Although not all features that are in the US are available in the other countries. The number of users is growing quickly as in 2017, it was reported that they only had 7 million active users.

In the pandemic, it seems CashApp has only accelerated growth as drivers such as a younger investor joining the stock market and stimulus checks have really helped the quicker adoption of the app. In the last quarter (Q3 2020), the company reported that daily transactions doubled compared to last year and that the stock brokerage is the best product in terms of performance from the first months since launching a product.

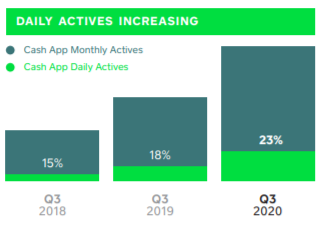

There is also a clear trend that people are not using CashApp just for P2P anymore, and daily activities are increasing fast in the last years:

Source: Square Q3 earnings report

It is also important to note that Bitcoin is a big part of CashApp as well. The company reported $1.6B in revenue generate through serving clients with Bitcoin transactions. The company breaks down this revenue as it would otherwise make the business segment's analysis really hard. Even though they say that they do not make much money on Bitcoin trading the Bitcoin segment earned $32 million in gross profit in Q3 2020. When looking at the volume, it is not “nothing” as it presents 2% of the revenue from Bitcoin trading.

What is more impressive is looking at their financial data:

Source: Square Q3 earnings report

Cash App revenue, excluding Bitcoin, earned $434 million in Q3 2020. This is a growth rate of over 150% YoY. Even if we zoom out and look at the last 9 months, the growth number doesn’t change much.

Most of the revenue of Cash App comes from the Subscription and service-based revenue segment. Even more impressive is looking at this segment as consolidated results for the whole company:

Source: Square Q3 earnings report

The revenue from subscription and service based revenue in Q3 2020 was $447 million while the cost of revenue was $66 million, so the gross margin in this segment was 85%. What is even more interesting is that last year the cost of revenue for this segment for the same period was $63 million, with revenue only at $279 million. This shows how much more profitable Cash App is becoming with scale.

While Square does note that the last results are somewhat elevated because people receive stimulus checks on their Cash App accounts, the trend cannot be denied.

Cash App hasn’t even rolled out features like loans. So far, it is testing offering small loans to a small number of accounts, but looking down the line, they can fully replace what a bank offers nowadays and more.

In these times, we can clearly see that a younger generation of people investing and using financial services is here to stay, and Cash App, together with some other FinTech products, is their go-to platform.

Competitors on Cash App

Ok, so looking at the competition, there are quite a lot of Fin-Tech apps out there. The main competitors for me are Venmo, Zelle, and SoFi.

In terms of Venmo, if we had this conversation 1 or 2 years ago, my thought might be different, but now I think Venmo is starting to lose the race against Cash App.

The main reason Cash App is performing better, in my opinion, is because it offers more features (and offers them sooner than competitors). The way Square is looking at P2P (merily as a source to gain new customers) is the right way. With Venmo, there are still a lot of people using it only because of P2P. The other thing is Cash App is so aggressive in marketing. In fact, I would argue their marketing is one of the best I have seen. And another important fact to consider is that because of Square’s B2B business, Cash App can offer perks to their users such as Boosts or discounts for places such as restaurants or bars. An interesting feature is also that you can receive your paycheck directly to Cash App.

This chart also shines some light as we can see that Cash App has really outperformed Venmo since April 2020 in terms of search in the US.

Source: Google trends

When looking at SoFi, they have a much lower user base so far, but the main thing Square must watch out for is the fact that SoFi also offers loans to their clients. This is a business segment in which SoFi has experience because of its core business. But with Square testing the loan feature already, I think they will be able to roll this feature out soon.

An important milestone for Cash App will also be an expansion into Europe. And while there are many smaller competitors in Europe, Square is taking the first steps in the market. In their last earnings call, they told us that they recently acquired a Spanish startup called Verse to learn about the market. So it seems expansion into Europe is not far away.

Valuation

Valuing Cash App is a more challenging task. Normally I would look at the active user number and user growth, and the value of one user in the fin-tech space. But since we don’t have accurate information on this part, we can only value it through current financial numbers. This means that we take into account only the products and services that the company is currently offering and do not take into account the potential of new products the company can offer to increase the ARPU.

The numbers show us that Cash App revenue on an annual basis should be around $1.7B, they have a crazy gross margin of over 80%, and they are growing 150%. While it is hard to estimate if this company was trading as a stand-alone company I think at current market conditions, the market would easily apply a 50 times P/S multiple, given the high margin, high growth rate, and fintech space. The estimated value of this business given these multiples would then be $85B.

Synergies between both ecosystems

While I evaluated both of Square’s business segments separately, both businesses combined offer many synergies and support each other. To provide some examples.

Companies that use the Square seller ecosystem can pay their employees directly to Cash App. This can motivate employees to open a Cash App account and get their salary faster.

Square can leverage their Cash App user base and provide their corporate clients access to Cash App users. The corporate clients get to offer their products and services to the whole Cash App ecosystem.

Company valuation

According to this analysis, the Seller ecosystem is worth $55.5B and the Cash App ecosystem $85B. If Square pays off all their liabilities, they are left with $0.5B in short-term liquid assets that we have to add. So the target value for SQ given all the above would be $141B or $312 per share. The stock is currently trading at $240.38 per share and a $108.4B market cap.

Summary

I think Square is in a unique position right now and has a competitive advantage, especially in the FinTech wallet space. The Cash App ecosystem will probably be one of the most important for them also going further but their B2B segment compliments their offering and provides good synergies. International expansion has just started in Square and will be a nice growth generator for the coming years.

Even though the stock had a nice run, I think the run is justified as their performance, especially in 2020, highlights their strong market position and I believe in the company long term.

If you liked this analysis and are interested in others, please subscribe to this newsletter; it is free. I also regularly post my portfolio positions and the investment moves I make.

Disclaimer:

Nothing contained in this website and newsletter should be understood as investment or financial advice. All investment strategies and investments involve the risk of loss. Past performance does not guarantee future results. Everything written and expressed in this newsletter is only the writer's opinion and should not be considered investment advice. Before investing in anything, know your risk profile and if needed, consult a professional. Nothing on this site should ever be considered advice, research, or an invitation to buy or sell any securities.