The inevitable Tech Clash: Chip designers vs Computing platforms

Welcome to UncoverAlpha newsletter. The newsletter is primarily focused on sharing my analysis and insights on great companies in the tech and growth sector. The newsletter is free, so if you haven’t, you can Subscribe on the following link.

This article is sponsored by Masterworks.

As part of writing UncoverAlpha, I get to learn about amazing tech companies being built. I never forget the true disruptors. Today’s partner, Masterworks is one of those companies. This revolutionary fintech startup lets you go beyond traditional assets and lets you diversify your portfolio with multi-million dollar paintings. When I realized blue-chip art prices outpaced the S&P 500 by 164% from 1995 to 2021, art investing really caught my attention. In fact, I just signed up for Masterworks. If you’d like to join me and 330,00 members on the platform, click this UncoverAlpha link for priority access.

*See important disclosures

If you are interested in sponsoring the next article, you can DM and reach me on Twitter @RihardJarc

Hey everyone,

In today’s technology era, most people cannot imagine living & working without technology. Especially after the pandemic, the adoption only got faster. It even caught up to the people that were not tech-savvy and were still fighting the trend. One of those “fighters” was my mom. Because of work from home and the everyday use of apps to go to places and show your vaccine certificate, she had to adapt and get a smartphone, and she actually knows what Zoom is now. But what was so interesting for me was watching her adoption curve. In a few weeks, she went from only using the smartphone for these “necessities” and calling it a device that makes people more stupid to using the smartphone now in her spare time (solving crossword puzzles on the phone, watching the weather, news, etc.).

The inevitable thing is that our lives will be even more affected by technology in the coming years than now. And one of the strongest trends in tech is the adoption of the cloud and the high need for chips, sensors, and GPUs to power all the gadgets, items, and apps we use daily.

And here we come to the backbone of the whole tech world: computing platforms and chip designers/manufacturers. Without them, nothing would work.

Because of the recent chip shortage that has been going on for almost two years now, cloud computing companies saw how dependant they are on the chip providers to continue to grow their datacenters and power their computing platforms. With the fact that companies like Nvidia and AMD mainly do not manufacture their own chips and GPUs but rather design them and outsource the manufacturing part, cloud computing platforms from companies like Amazon, Google, Alibaba, and others started to skip the design companies and went to the manufacturers directly in their ambitions and efforts to build their own chips.

If we also look at the chip and GPU designers like Nvidia, they are also starting to get more hungry with their saturated market and began exploring options to increase their TAM and provide other services such as computing services.

The semiconductor market

For the base understanding of the chip market, we have three types of companies:

chip designers

chip manufacturers

hybrids

While most people know this by now, many companies, whom we perceive as chip manufacturers, are actually chip designers. Examples are Nvidia, AMD, Qualcomm. The chip designers design the chips, but the manufacturing is outsourced to chip manufacturers/foundries. The main reason for this arrangement is that chip manufacturing requires constant high investments in building the foundry (manufacturing process, equipment & plant) in keeping up with the newest, smallest, and most effective chips. It is still essential to understand that chip designing is a complex and high CAPEX (Capital intensive) business in itself and that designers and manufacturers usually have long-term and strong relationships.

Chip manufacturers are the companies that manufacture the chip. Two of the most important chip manufacturers globally are Taiwan Semiconductor and Samsung. Even if we look at chip manufacturing on a country level – Taiwan and South Korea represent 80% of the global chip manufacturing. With the chip shortage and understanding the importance of chips on the whole economy, countries like the US and China are pushing to increase and build up their homegrown chip manufacturing.

Then we also have hybrids. These are the companies that design and manufacture their own chips. An example of this is Intel. They both design and manufacture their own chips. But the company has had trouble catching up with competition because they fall behind on their technology of developing 7nm and 5nm nodes.

To understand how Capital Expenditure (CAPEX) intensive it is running a chip Foundry we can look at CAPEX spend of the three key players for the last years:

2021 CAPEX of Foundry:

Taiwan Semiconductor (TSMC) $28.5B

Intel $18.3B

Samsung Foundry $8.6B

And the CAPEX looks even crazier when you look at estimates from these companies for this year:

TSMC almost $33.9B

Intel $26.2B

Samsung Foundry $11.9B

For comparison, the combined CAPEX spend of all three companies in 2019 was $35.1B, and now we are talking about only company - TSMC spending almost that combined amount in 2022.

Market share

To understand the market share, we first have to break down the market to chip manufacturers (Foundries) and then to CPU and GPU designers.

In terms of Chip manufacturing, the recent estimates are the following:

TSMC – 54% market share

Samsung – 17% market share

UMC – 7% market share

Global Foundries – 7% market share

SMIC – 5% market share

So, in reality, we can see that the two companies control almost the whole chip manufacturing market.

When we come to the market share of GPUs, we have to differentiate between integrated GPUs in computers where Intel owns the market and so-called “stand-alone” or discrete GPUs where Nvidia and AMD own the market (although Intel is about to enter this market now as well). In the discrete GPU market, Nvidia has 83%, and AMD has 17% of the market share.

Why is there a shortage?

To put it as briefly as I can, it’s a consequence of the pandemic and bad planning. When the pandemic started, it was a total shock to the whole economy, with the worldwide lockdowns. Factories that produce chips were affected by the lockdowns as well. And in the first early days of the pandemic, consumers were insecure. Everybody was expecting that consumers would act more scared and that consumer sentiment would fall. But after a few weeks, the opposite happened.

Because of the pandemic, consumers started buying a lot more IT stuff. From computers to gaming consoles and all other IT gadgets. The main driver was, of course, working from home, and people being bored in lockdowns, that's why they started to play many video games, watch movies, etc. Because of this massive demand for new IT gadgets, the need for chips soared. Months later, consumers expanded from just buying IT gadgets to buying cars, etc. The helicopter money (fiscal stimulus) helped lift consumer sentiment, so people started buying everything. And nowadays many products including cars have many chips in them. Businesses also migrated their IT infrastructure to the cloud, because it is easier to manage your workforce and work with clients with your IT infrastructure in the cloud. Again causing more demand for data centers and computing services that need many chips. Then came the third wave. Soaring prices of cryptocurrencies. Again, as we saw in 2017, this lead to the increased demand for chips from cryptocurrencies miners.

So the significant, unprecedented demand for products together with the world’s soaring demand for adopting technology resulted in a world chip shortage. The fact that 80% of world chip production comes from two countries didn’t help (Taiwan and South Korea).

And because this demand hasn’t really reduced when the economies are still faced with waves and waves of new covid strains and because building new foundries takes at least two years to set up, we are still facing the shortage. Given the past experience of demand-supply cycles, chip manufacturers are also hesitant to build too much supply as they are afraid of the bullwhip effect. Today, everybody is overordering their chip orders because if they stated the actual amount of chips they need, they would not get the order filled anyway. So they overstate. But this results in skewed orders and an overstated demand for chips.

The shortage is not affecting all industries equally, though. The gaming providers are better off because of their longstanding relationships with the foundries, while an industry like auto manufacturers is having a more challenging time because they are relatively new customers to the chip manufacturers and do not have yet close longstanding relationships.

Is Moore’s law dead?

In 1965 Gordon Moore observed that the number of transistors in a dense integrated circuit would double every 18 months. He later revised that to 24 months. Three years later, he co-founded Intel, and his observation was the benchmark for the semiconductor industry for decades. This “law” is important because it basically meant that approximately every two years, personal computers and other tech devices could do twice as many new and unexpected things as before. But the problem is the size. The primary method has been to make transistors and the wires that are transmitted smaller and smaller. But when you have smaller and at the same time faster components on a computer chip, it will generate more heat and potentially melt.

While I wouldn’t call Moore’s law dead just now, it is definitely slowed down a lot since we have a limited way to go in terms of shrinking the size of chips, the production is getting costlier with every new generation, and at the same time, we are limited with the speed of light. We will bump into Heisenberg’s uncertainty principle. And because of this slowdown, you can understand that the chip designers are starting to look for new segments on where growth will come from.

Cloud computing platforms

Computing platforms are the second backbone of the software world. Their main goal for their customers is to provide the environment and resources in which software can be executed. They make it so that their customers do not have to build expensive IT hardware infrastructure and are one of the primary reasons why so many young companies that have SaaS business models can get started and can scale.

The biggest cloud computing platforms in the world are AWS from Amazon, Azure from Microsoft, Google Cloud, and Alibaba Cloud.

What services do they offer?

We can break down the services these platforms offer into four categories:

Storage – storing data

Computing services – lending out computing power (CPU, GPU, etc.)

Networking services – Virtual routers, load balancers, VPN, etc.

Other SaaS services – various SaaS services like Elastic search, APIs to help with AI models, some are owned by the platforms some are offered from their software partners)

But the important thing to note is that while Storage and Networking services are great business segments with stellar growth projections for the coming years, the computing service and Other SaaS services are where the real growth will come next.

It is a trend that has already emerged that is why you see more cloud computing giants offering their own versions of popular SaaS services as they want a position themselves where the growth and profit will come for the coming years. Services such as MongoDB, Elastic search, etc.

The fight for having the best computing platform is also a big one and is already in the works. With the world turning more online and with the Metaverse concept, the need for computing increases exponentially, and the need for computing platforms with it.

Since the companies do not break down the profitability and revenue of each service inside the cloud unit, it is harder to get an accurate state of the market and the segments. Still based on estimations from different industry insiders, here is an interesting overview of the market leader AWS and the breakdown of their services.

It is estimated that AWS still makes about 70% of its revenue from two of its basic services. Storing (called S3 and EBS) and computing (called EC2). For the EC2 product, the gross margin is expected to be in the range of 50’s, and for S3, the gross margin is in the range of 50-70%. But what has constantly been growing in terms of % of revenue is the “other SaaS services” segment, which has a higher margin. But with the SaaS segment, we need to understand two business models. One is where AWS offers its own SaaS service to the client, and the other is where the clients use third-party SaaS services through the AWS marketplace. Estimations are that AWS charges an average 5% fee on listings. The marketplace fees are considerably lower than what companies like Apple and Google charge in their app stores, where the fees are as high as 30%. For its Azure cloud platform in the summer of last year, Microsoft reduced its marketplace fee from 20% to 3%, showing a considerable willingness to compete in this important market segment for the future.

What is the market share of the sector like?

The market is dominated by Big Tech players that have big pockets to be able to fuel the investments:

The dominant platforms are AWS from Amazon with 32% market share, Microsoft Azure with 20% market share (although they are now probably catching up to AWS), and Google Cloud with 9% market share.

They are followed by Alibaba Cloud, IBM, Salesforce, Tencent cloud, Oracle, and companies like Digital Ocean.

The Clash

Now let’s get to the heart of it all: the clash between chip designers and computing platforms.

Back in the day, there was a straightforward exchange happening. Cloud computing platforms were buying chips from chip designers, and the chip designers were either manufacturing their chips or outsourcing the manufacturing to foundries. And that was it. A very clear relationship between what each party offers in terms of services and who the buyer & supplier is. But this is not the case today.

I made this visual to understand better what is happening in both of these markets and how they are connected today:

Today we have cloud computing companies buying chips from chip designers, but at the same time, they are also developing their own “inhouse” chips with the help of a company called Arm Holding. Arm holdings sell/licenses chip designs, which computing platforms can then use to order the custom chips directly from foundries (skipping the traditional chip designers). Arm Holding is the company that Nvidia wanted to buy from Softbank but didn’t get regulatory approval. I am sure now you all understand why Nvidia wanted to own this company so badly and what it would mean for Nvidia. If they were successful with the deal, they would have successfully “hedged” their business and benefit in “every way” the market would develop.

While most computing platforms explain this move to go direct to Foundries because they want more custom fit chips for their data centers to better power AI training and stuff like that, I view this as only the first step for them. Computing platforms will want more and more of their chips to be built in-house to control this vital part of their service and increase their profits. A lot of the reasons why computing platforms can also do this is because they have bigger market caps and have larger amounts of capital at disposal than the chip designers.

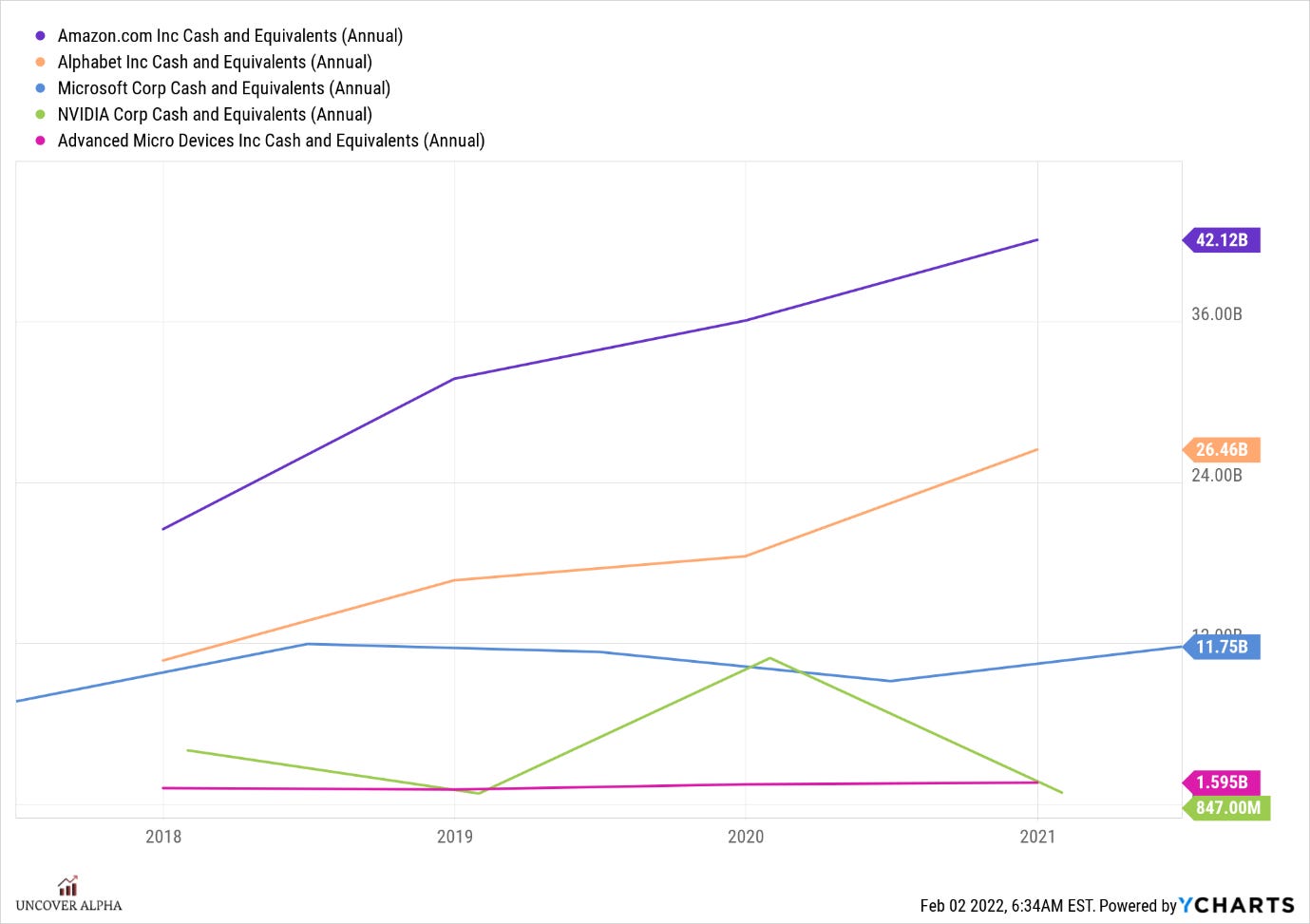

When looking at the Cash on the Balance sheets of companies like Amazon, Alphabet, and Microsoft, we can see how big of a difference it is compared to chip designers like Nvidia and AMD. That is why it is not a big problem for computing platforms to channel some R&D funds to chip design and compete with their suppliers.

With this change in the market by computing platforms, Chip manufacturers/foundries like TSMC and Samsung have expanded their client base. They are getting direct orders from clients like Amazon, Microsoft, Google, and not to forget Apple.

But the recent rise in the market cap of many chip designers might help them in the long run if they can sustain these levels if they want to raise capital and invest more in their computing segments.

The last important part of the semiconductor chain is a European company called ASML. They are the most important manufacturer of extreme ultraviolet lithography machines that are used in the production of chips. And because of their next-generation machines that have previously unattainable levels of precision, they have entirely cornered the market. Each machine costs roughly $150 million and is the size of a bus. The company and its machines are among the most important assets in the semiconductor industry and manufacturing process. And as you may expect, ASML, because of its role, is not a small company. In fact, it is one of the top 5 biggest European companies by market cap at $258B.

Chip designers also have bigger ambitious

The other side of the clash between chip designers and computing platforms is because of chip designers. Companies like Nvidia have now seen that they too can skip the “middleman” in their process, which is the computing platform, and offer computing services powered by their GPUs directly to developers. An example of this is Nvidia’s recent Omniverse platform and its’ Deep Learning Inference Platforms.

For those of you who do not know what the Nvidia Omniverse platform is yet, this short video summarizes their efforts very well:

While the Omniverse platform is still primarily used for rendering and 3D simulation, you can see that this is not the end goal and that a full-scale computing platform is the end goal. And with so many big tech companies acknowledging that the metaverse, AR, and 3D is the next computing platform, you can understand that the big computing platforms won’t leave this space untouched and will want their piece of the pie.

The other big platform Nvidia is building is the Deep Learning & Inference platform, which is already in direct competition with the big cloud computing offerings. Inference is a term used in the software AI space as a process of taking an AI model trained beforehand (for example, with deep learning methods) and deploying that model onto a device that will process incoming data to enhance itself and make the algorithm more accurate. It is essential in the process called at the Edge. This means that data needs to be processed in real-time, and the AI model needs to produce results as fast as possible. That is why with Edge processing, the data isn’t transferred to the cloud to be processed, but instead, there is usually a low-power computer with an integrated inference accelerator, close to the source of data so that the results get processed as fast as possible.

Inference will be used more and more in the future as good AI models will need to receive and train from new incoming data and modify constantly. Also, processing at the Edge is a fast-growing field, especially with the Autonomous driving business segment where microseconds decision can make a life-changing difference.

Summary

So, if you are asking yourself why it is important to understand this dynamic happening in the semiconductor and computing space, let me give you the answer. It is important to understand this even though right now we have a chip shortage, and it might seem to investors that every company in the semiconductor space is a great idea. I believe it is imperative to understand where the industry is going and not where it is now. All that said, I think these two sectors will, in the end, merge and form a “super” chip computing company. These companies will control both aspects of the business (chip design and a computing platform) because it makes sense from a position of power/control and a profit standpoint. As an investor, It is wise to think about which companies will come “on top” and which will have problems because of this new order.

If you haven’t yet, feel free to subscribe to this free newsletter & share.

Also, if you liked some of the charts in the article, they were made by the Ycharts tool. Go check it out.

Disclaimer:

From the companies mentioned in the article, I own Google & Amazon.

Nothing contained in this website and newsletter should be understood as investment or financial advice. All investment strategies and investments involve the risk of loss. Past performance does not guarantee future results. Everything written and expressed in this newsletter is only the writer's opinion and should not be considered investment advice. Before investing in anything, know your risk profile and if needed, consult a professional. Nothing on this site should ever be considered advice, research, or an invitation to buy or sell any securities.