Why Facebook is one of my main Portfolio positions - analysis

Facebook is one of those companies and stocks that are getting a lot of heat and hate in recent months. Nonetheless, it is one of my core positions, and here is the investment thesis behind it.

The general

To fully understand FB, you must first understand that this is no longer just the “blue Facebook” company. Facebook has built, over the years, one of the strongest digital assets in the world.

The main way to segment Facebook is:

“blue” Facebook and Messenger

Instagram

WhatsApp

Facebook Reality Labs

Now I will not write general presentation like descriptions about these segments as I believe that won’t add any value as most of you probably know them. I will dive into each of these segments and bring you the data and things that I believe should not be missed and should be known when investing in FB.

“Blue” Facebook

This is one of the most “hated” parts of Facebook and that most bears focus on. This is the part where everybody likes to call this is the dead FB segment. But if we look at the numbers, this “dead” part is not dead at all:

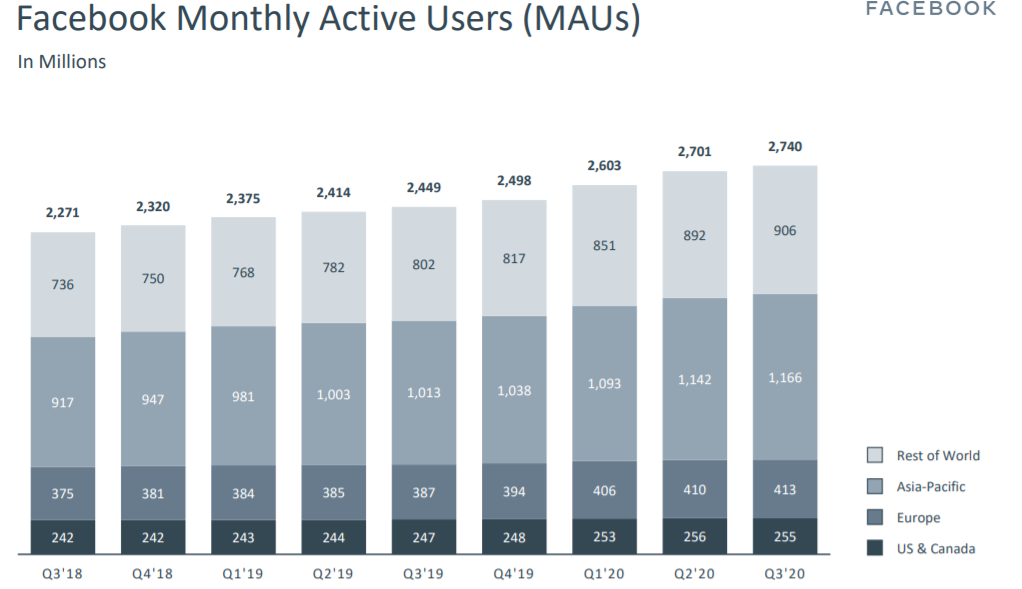

1.8 billion people are using it daily, and 2.7 billion people are using it monthly. And we can see that it is still growing, although be it at a small percent (because of the sheer size). It is important not to be blindsided because you may represent a younger population that nobody is using it. Again 1.8 billion people use it daily, and these are people that still hold much of the buying power.

And this huge user base is currently being monetized by one source, and that is advertising. Facebook as a company made $70.7B in revenue in the year 2019, although Facebook doesn’t break the revenue from the “blue” part and Instagram, there are estimates that out of that the “blue” part generated $50B. Looking at the numbers, the Gross Margin is more than impressive. Even at this scale, it stands at 82%. So this is one of the most profitable businesses in the world.

Now the “blue” part of Facebook serves for two important things, in my opinion. One is it is the “cash cow.” It generates huge amounts of cash that can fuel other parts of the company. The other one is its huge user base can provide a great source of upselling other services besides advertising.

I like to invest in companies with big user bases because doing an upsell to your existing client base is much easier than going “on the market” and paying to acquire new customers.

Instagram is the more “cool” part of Facebook. Facebook acquired Instagram in 2012 for $1 billion. When FB bought Instagram, Instagram had roughly 50 million users. In 2020 this figure is said to be around 1 billion. Back then, it also didn’t generate any revenue. In 2019 it was rumored that Instagram generated around $20 billion in annual revenue.

The main thing about Instagram is the potential it has in social commerce.

Social commerce is a concept that is very popular in the East with Pinduoduo, Alibaba, and others in China, Sea Limited in South East Asia, and others. Social commerce means that the user of social media makes an e-commerce purchase inside the social media app. So this is a more interactive and personalized experience of e-commerce. I believe social commerce is already and will be even more important in the West in the following years.

There are two key “social assets” in the West that can currently offer a perfect social commerce experience. One is Pinterest, and the other one is Instagram.

Instagram is built so that the visual presentation and visual elements are more important than the text and words. It is also the most important “home” of social influencers. Social influencers, either big ones or even micro-influencers, are a trend that is driving a lot of sales in the e-commerce and marketing space.

It is key for Facebook to make sure that Instagram stays “cool” and keeps the market leader position in the influencer category. This is what keeps the users on the platform and drives new ones.

Instagram is a platform that needs to focus mostly on user growth and user retention. Simultaneously, “blue facebook” can be more orientated towards businesses (so the customers that pay for ads and e-commerce features). That is why Instagram also needs to keep up with the competition on the feature front, be it with the Story feature (first introduced by Snapchat) or Reels (first introduced by TikTok).

Instagram is Facebooks’ crown jewel on the social commerce part. At some point, I believe it will generate more revenue from commerce features that advertising.

Another important acquisition company of FB is WhatsApp. Facebook acquired the company back in 2014, which was then an eye-popping $19 billion valuation. One of the first things FB did was get rid of its annual subscription fee of $1 and made the app free. The app has surged in popularity, especially in emerging markets like India. WhatsApp has around 2 billion users now and is an essential part of the FB portfolio.

WhatsApp was able to be free and unmonetized all this time because it was “fueled” by the cash cow of FB’s other operations. FB recently announced goals to start monetizing WhatsApp, although the strategy, in my view, will be different from the classical advertising business.

WhatsApp has the ability to become one of the key fintech and e-commerce apps (similar to WeChat from Tencent in China). When the cryptocurrency backed by the association of companies, including Facebook, launches Diem (the cryptocurrency), WhatsApp could serve as the main front window to the cryptocurrency wallet Facebooks wants to launch called Novi, which will be able to hold Diems. Also, WhatsApp is providing a key bring between businesses and clients in terms of communication. FB is now rolling more and more features that are orientated to help businesses attract WhatsApp users and sell them products through the chat. We can see that FB is going in the direction that Square has gone with its ecosystem – connecting their sellers who use Square with CashApp users. I think FB is going in similar directions. The latest acquisition of CRM startup Kustomer (for $1 billion) is a sign of this. Kustomer will provide the businesses that use WhatsApp, features for better managing potential clients (WhatsApp users).

WhatsApp recently announced new privacy changes, which mean more information sharing with its mother company Facebook. But there are no changes to end-to-end encryption, although many people on social media have been claiming this. We also saw many people calling this the end of WhatsApp and going to platforms such as Signal and Telegram. But the fact seems not to tell this story.

According to Adam Blacker, vice president of insights at Apptopia, despite the surge in Signal and Telegram downloads, WhatsApp has not seen a decline.

“It’s too ingrained. My guess is there is a very small number of people who use WhatsApp daily that are recently deleting it,” Blacker told CNBC by email. “Even those who are downloading and using Signal or Telegram will continue to use WhatsApp as that is where most of their friends and family are. They may start to talk to certain people on Signal but still chat with their mom on WhatsApp.”

Facebook Reality Labs

Not many people know this segment of Facebook’s operation. But this is one of the key business segments for Facebook’s long-term growth.

Facebook Reality Labs is a business segment where FB develops VR and AI solutions. These range from software things to hardware (Oculus and AR glasses).

FB is investing heavily in this business segment, as Zuckerberg believes that AR/VR is the next “platform” similar to smartphones. I share his belief that especially AR, has the potential to become the next big platform.

To understand the magnitude of this segment, we need to understand where, despite being extremely powerful and strong, FB lacks others. It does not control the hardware and, with that, has the whole ecosystem. One of the main things FB has trouble with is that it does not own the operating system and app store. So it is as every other developer company out there depended on the Apple and Google ecosystem. That brings a problem for FB as both Apple and Google can dictate policy changes, in-app-purchase fees, etc. Zuckerberg knows this, so he wants to be prepared when the next platform becomes mainstream to own the whole ecosystem and not be dependent on other companies.

So in this segment, there are two important things: VR (Virtual Reality) and the other one is AR (Augmented Reality). To put it as simple as possible, VR means that you enter a complete virtual world (virtual environment). AR means that the environment is the same as the real one but that things are projected into your environment (through holograms).

This is really life-changing technology, and if you are interested more in how Zuck sees it, this is a good video to start: Talking Tech and Holograms with Mark Zuckerberg!

FB shows a high understanding of how AR and VR can become the next platform.

In terms of VR, they sell their Oculus VR headsets. They recently reduced the price of their new set to under $300, making it very affordable. Zuckerberg talked on many occasions that their goal is to get 10 million people active on this “platform.” This is what they calculated as the critical mass for the product to go mainstream. The key thing is that with an ecosystem of 10 million users, developers start to enter a platform and produce features, content, etc. This is because developers need to see enough mass in users to make features that people will pay for and make a business out of it. FB already has developers working on their platform, but so far, they are mostly being “financed” by FB.

And then there is the AR segment, which, in my view, has even more potential to become the next platform. Here they are developing AR glasses. They are very strict on what for them the product should look like. The glasses should be as slick as possible and resemble ordinary glasses or sunglasses (with a thicker side). A key decision here is when they partnered with Luxottica, which is set to start in 2021. Luxottica is the leading manufacturer of glasses and sunglass. From Ray-Ban, Prada, Versace, and more. So this means that FB knows that for people to use AR, the glasses need to look like ordinary glasses we wear now and be cool. Nobody wants to look odd when walking down the street.

But these “moonshot” projects, if you will, are not that far away from reality. In fact, if you look at the last four quarters of FB’s Other Revenue segment, which is mostly Reality Lab, it makes $1.2B in revenue on an annual basis. The YoY growth of this segment is also high in the 40%-60% range. So if this was a stand-alone company, the valuation of this wouldn’t be small for sure.

On the flip side, everything that FB is developing in this segment, in terms of holograms and visual tech, can also be used on their social media assets like Instagram (which is more visual-based). So the R&D FB is paying will not reap the results only when AR/VR becomes mainstream but will also provide competitive advantages in a short time frame to assets like Instagram.

Financials

Ok, let’s look at FB’s financials.

Source: yahoo finance

We can see that before COVID, the revenue growth was 37% in 2018 and 26% in 2019. This year because of COVID affecting many small-medium businesses, advertising growth will be in the mid to low teens. Nonetheless, even in advertising, FB has been gaining market share in the last years.

What is even more impressive is the Gross Margin that is constantly over 80%, which shows just how profitable this business is.

One important thing to notice is also Operating Expenses. They have been rising fast, especially in the last 3 years. The main reason for higher Operating expense costs is administrative costs related to content moderation. So the push to moderating and removing inappropriate content has affected FB’s business in the last years, and this trend will probably continue. Although FB wasn’t that prepared for this a few years ago, they have probably invested a lot into R&D in terms of software on this segment to reduce the human labor costs associated with this.

Main challenges

The main short to mid-term challenges FB is facing today are, in my opinion, the following:

Possibility of regulators to push for a company break up

iOS new privacy tracking update

Repeal of Section 230

Now while I won’t give you a deep dive on my thought process for each of these challenges, I will give you my end conclusions on them.

Possibility of a regulatory push for a company break up

I find the possibility of this happening low.

The main reason:

Questionable political support to go all the way

Legal challenges for the government to build a strong case

FB will fight it hard

The US is in a tech war with China and crippling your main players is not a good strategy

While each of these points has the potential for a new post, I will leave it at that.

Even if, in some scenario, the break-up would happen, I believe current FB shareholders would get more value than what the FB’s market share is currently reflecting (look at the Valuation part).

iOS new privacy tracking update

Apple introduces its plan for a big privacy change in which users will be asked if they allow a certain application to track them while they are not using this application. So this means that now, for example, FB could see what other apps users have installed and, for example, what sites the users visited, etc. There was the optionality for an iOS user to turn this off, but it required the user to go into Settings. Now a pop-up will appear once you start using an app. FB acknowledges that this change will have a material effect on their clients. So this is a challenge as many users could choose the “not allow” button, and with that, FB will have less information about the users.

This is not a problem that is FB specific. With that, I mean, is that the whole sector will have the same challenge. In general, online advertising will become less effective for advertisers as advertising platforms will have less information resulting in less effective targeting.

With this change, I don’t think it will much affect FB’s business as advertisers will have the same challenge on every platform they go to. So the end result could be lower efficiency of advertising campaigns, but the market positioning in the industry should not change. In a sense, FB may even get more advertisers as data they gather in their internal ecosystem may become even more valuable.

Repeal of Section 230

So Section 230 is legislation that basically provides immunity for website publishers from third-party content. So in a sense, it protects platforms from being legally responsible for the content that their users publish (there are some exceptions).

There was a political push to change this right before and after the recent US elections. This push may continue going forward and present a challenge that platforms might have to address.

Mark addressed this challenge in the recent earnings call:

“So at this point, we have the benefit of seeing how different countries have adopted different types of regulation and getting to understand how that either makes the problems more effective for dealing with them or, in some cases, makes it harder and actually creates worse results. So the approaches that I think seem to have worked best by looking at what France and a few other countries have done is basically one which focuses on creating a transparent process where companies have to report how they're doing moderation, reporting on how much harmful content of different categories is visible, the portion of the content on the service, and what percent of it our content moderation systems can get to before people need to report it to us. And I think a system like that, which basically requires companies to meet certain thresholds or show improvement, aligns incentives in the right way to encourage companies to minimize the amount of that harmful content that people are seeing. But there are plenty of examples where there are other regulatory regimes that I think point towards -- that are counterproductive, right? Or basically require companies to do things that aren't quite getting at the most important aspect of the problem. For example, in some countries, there are rules saying you have to get to certain content within a short period of time. And that, I think, is good on its face, but I think the reality is that a piece of content that's going not to be seen by many people, maybe it's not as urgent to deal with as one that is going to be problematic but is going to be seen by a lot of people. You really want to get to that sooner. So treating all content equally compared to just looking at the prevalence of how much bad stuff people see I think is going to be less effective overall.”

FB is, in my opinion, one of the most prepared companies for this kind of change. It also has the most resources to comply with it, and again this change would affect the whole industry. In the end result, I think this might even help FB as competitors will have higher entry barriers and will have to spend a lot of resources and cash to have departments that will moderate content and keep it in line with the possible new legislation.

Main opportunities

Diem and cryptocurrency

Facebook has started an association to form a cryptocurrency. Now this project was first named Libra, later changed to Diem. The purpose of the association is to form a network of partners who will support the cryptocurrency. The cryptocurrency is proposed to be a stable coin backed by the USD (although there were plans for it to be backed by different fiat currencies). The partners in the association are powerful, reputable companies. To name a few: Uber, Lyft, Shopify, Spotify, PayU, Coinbase.

So while FB will not own the currency, their company Novi will launch a Wallet that will hold the cryptocurrency.

Now make no mistake; this is a huge thing for FB. If they apply the wallet through all of their assets (Instagram, Messenger, WhatsApp, etc.), they leverage their huge user base and make it for people to have an easy way to buy things, send P2P money, etc. They basically make CashApp but with a currency (Diem) that means fewer transaction costs and no more credit card fees. With their partner network, this is even a bigger deal.

Imagine ordering an Uber and just paying through Messenger or WhatsApp. This would present a real disruption to the whole FinTech world, as FB has the biggest user base out there. And people will adopt it because all of their friends will have it from day one (because they use one of FB’s assets), and it will be the easiest way to transfer money.

Also, for developing countries with high inflation, this is a game-changer. People will be able to transfer their local currency to Diem (which is stable in price because it is USD backed) and not worry about the bankruptcy of local banks or local currency inflation.

Now Diem faces and still will face a lot of pressure from governments worldwide, as many see it as a threat to their financial system.

AR/VR

The AR and VR segment is one of the biggest opportunities for FB as it is the biggest investor in the world in terms of AR/VR. If this becomes the next platform, FB has good chances to become the leader in this space.

Social commerce

We already discussed the capabilities of FB to be able to leverage their assets and build a unique commerce experience. I believe FB is in the early stages of this social commerce adoption and will be a completely different company in the next 5 years. I expect a big portfolio of the revenue to come from none ad-related segments like Social Commerce.

Zuckerberg

While some dislike him, you have to give him the credit he deserves. He is one of the youngest “big tech” founders of the decade and is exceptional in execution. The acquisitions of Instagram and WhatsApp are one of the greatest acquisitions of all time.

He knows how to protect FB shareholders from competitive threats. This is either via M&A either via copying features from other platforms; thus, he keeps the FB family of products always competitive. We know what happened to MySpace and FB with Zuck in charge seems like a completely different story.

Valuation

Ok, so from a valuation standpoint, the stock is currently trading $251.36 or, to put it in market cap at approx $ 716 billion.

Now, if we try to evaluate FB’s business segments:

“blue” Facebook – in 2019, Instagram is rumored to have produced $20B revenue, so the “blue” FB made around $50B in revenue. In the last 3 years, FB’s pre-tax net margin has been around 50%-30%. If we take 35%, which was the latest info, because of higher costs (mostly related to content moderating), that means that the “blue” business segment is netting pre-tax $17.5B in profit. Now since this is a mature business, a P/E multiple of 20 would be appropriate. This would value “blue” FB at $350B.

Instagram. Instagram has said to produce $20B in revenue in 2019. It has also been consistently growing more than 30% on the top line. Considering the growth and the high gross margin business, a 15x Sales multiple seems reasonable. This would value Instagram at $300B.

WhatsApp. So WhatsApp is a part of FB that is not yet monetized. But what we do know is that they have around 2 billion users. So let’s try to evaluate it based on the user base. It is really popular in the Asia Pacific and the Rest of the World, although many users are also in the US and EU. If we look at the ARPU breakdown of Facebook, we can see that they are monetizing the Asia Pacific users annually at $13.29 (data for last four quarters) and the Rest of the World ARPU at $8.47. If we average this number, we get to ARPU of $10.88. If we apply this ARPU to the user base, we get a potential annual revenue from WhatsApp at $21.76 billion. And let’s keep in mind we applied the monetization revenue of advertising, so we are not even thinking about other ways that WhatsApp can generate revenue. If we apply just a 10x Sales multiple to this business, we get a $217B value of WhatsApp.

Facebook Reality Labs. Now, this business is the one that is probably the hardest to evaluate. It has the potential to become the next “platform” but at the same time is a big cash burner in terms of R&D. What we do know about it is that the segment currently brings in approx $1.2B in revenue (data based on last four quarters) and that it is growing over 40% YoY. We also know that this is a mix of hardware and software, similar to a company like Apple. In current market conditions and because of its potential and growth, a 30x Sales multiple seems like a good start. That would value the Facebook Reality Labs business at $36B.

Now, if we add all the business values together, we get to $903B in value.

Now we must also take into account FB’s cash pile. If we take FB’s current assets and deduct all the liabilities, we get extra cash of $34B.

So together, my fair value of FB is $937B. The market cap is $716B. So in my view, FB has a 30% upside to reach a fair market value. But keep in mind that I valued FB’s businesses purely on advertising and didn’t even account for its potential to upsell other services like commerce features, payment, etc.

Summary

I recently added to my FB position as I believe the company is undervalued because of all the negative news. FB is one of the most profitable companies and is, in my view, a pure growth company. It is one of my core portfolio positions in the long run, and even in the short term, I believe there could be a big revaluation happening when they launch Diem.

If you liked this analysis and are interested in others, please subscribe to this newsletter. I also regularly post my portfolio positions and the investment moves I make.

Disclaimer:

Nothing contained in this website and newsletter should be understood as investment or financial advice. All investment strategies and investments involve the risk of loss. Past performance does not guarantee future results. Everything written and expressed in this newsletter is only the writer's opinion and should not be considered investment advice. Before investing in anything, know your risk profile and if needed, consult a professional. Nothing on this site should ever be considered advice, research, or an invitation to buy or sell any securities.

Superb write up, thank you Rihard!

Great analysis. Apple is the hypocrite here. If it really cares about privacy and choice, it wouldn't get the $12B annual payment from Google and it wouldn't kowtow to the Chinese government. Apple only does it when it doesn't affect its bottom line. Apple wants people to think it is on the moral high ground, but what it really wants to do is to disrupt FB's core business to slow down its development of the next potential computing platform (AR/VR) which Apple is currently falling behind. Right now, FB has the first mover advantage and can potentially build its own OS that's independent from Apple.

Disclosure: Long FB & AAPL